.jpg)

When you get your first paycheck, allowance, or birthday money, you'll likely hear, "Save it!" Others will tell you, "Invest it!" But what's the real difference—and more importantly, which one do you do first? Let's dive in.

Let us slide into your dms 🥰

Get notified of top trending articles like this one every week! (we won't spam you)Saving: The Safer Start

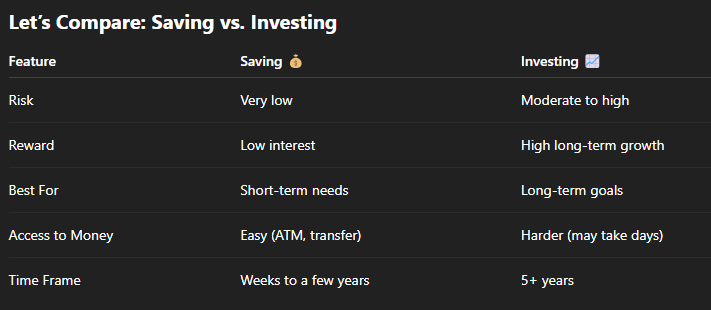

Saving is placing your money in a secure location, such as a bank account. It is money that you can retrieve easily and quickly. Consider saving as short-term funds, money that you may require in the near future for:

Purchasing a new telephone, emergency funding, a family present or trip, establishing a small company. Most teens start here because it's low-risk.

Your money doesn't grow much, but it's secure. A basic savings account earns a small interest (usually between 0.01%–1%), which means your money grows slowly. But it's growing nonetheless, and more importantly, it's secure and liquid.

Image Credits: Piggy Bank from Unsplash

Image Credits: Piggy Bank from Unsplash

Take the Quiz: What Creative Hobby Should You Try?

Looking for a way to express your creativity but not sure where to start? Then this is the quiz for you!

Investing: The Long Game

Investing is when you're placing your money in things such as stocks, ETFs, or real estate with the hope that it'll grow more in the long term. It's more risky, but with greater rewards.

- Let's look at the below:

- You Place $100 in a stock, and it grows 10% every year

- In 10 years' time, your $100 could be worth around $260

- In 30 years' time, it could be over $1,700

That’s the power of compound growth. But remember, investing also means the value can go down. Your money isn’t guaranteed, and there’s always a chance you could lose some of it. That’s why investing is better for long-term goals like:

- College

- A Car

- Retirement (yes, it’s never too early!)

- Building wealth over decades

Which Should You Start With First?

Here’s the honest answer: Start with saving. Then, move into investing. Why?

Your savings are your base. You would like to have a small "emergency fund" saved up before you begin taking risks with money in the stock market. Most professionals suggest saving at least $500 to $1,000 as a teen before you begin investing. Next, find out about investing little by little, even $10 or $20 at a time. Apps like Fidelity Youth, Greenlight, or Acorns Early let teens invest with parent approval. Just make sure you understand what you're investing in.

A Real-Life Example: Meet Maya

Maya is 16 and works part-time at a coffee shop. She earns $200/month. This is what she does:

- She saves $100/month in her savings account.

- Once she has $1,000 saved, she starts investing $50/month in a teen investing account.

After 4 years (by the age of 20), she has:

- Roughly $2,400 in savings

- Roughly $2,800 invested (and possibly more if the market goes up)

This balance helps her pay for emergencies and grow her wealth early on.

Image Credits: Andre Taissin from Unsplash

Why Teens Should Care

You might ask, "I'm just a teen. Why do I care?" But starting early is your superpower. The earlier you start, the longer your money can grow.

Let's say you only invest $1,000 when you're 16 and never add another dime. If it grows 10% each year, by age 66, that can become over $117,000. That's compound interest magic.

Common Mistakes to Avoid

Some traps beginners fall into include: Skipping savings: Don't invest a dime until you've built an emergency fund. Trying to get rich quick: Stocks are not lottery tickets. Be patient. Not researching beforehand: Always know what you're investing in.

Blindly following TikTok finance "influencers": Some offer bad or risky advice. Do your own research.

Image Credits: Chris Liverani from Unsplash

Final Decision: Start With Saving, Then Invest

To answer the big question, "Which do you start with?"—the answer is:✅ Start with saving to build security.✅ Then invest small for the future. You don’t have to pick one forever. In fact, the smartest money managers do both.

It’s not a race, it’s a journey. And the fact that you’re reading this means you’re already ahead.

Quick Tips to Get Started

- Open a teen savings account (check with your bank or credit union).

- Use a budgeting app like Rocket Money, Mint, or Greenlight.

- Read books like The Teen Investor or I Will Teach You to Be Rich (teen edition).

- Talk to your parents about the possibility of opening a custodial investing account.

Set a money goal: "I would like to save $500 by the end of the year."

Image Credits: Sortter from Unsplash

Closing Thoughts

Money is not only for adults. The earlier you learn how to use it, the earlier you'll be in charge of your future. No matter if you're saving for your first car or investing for your dream house, every sound financial decision starts with one question: "What's my goal?" If you have that, then you'll also know if you should save, invest, or both.

.jpg)

.jpeg)

.png)